Making money is always the market game, and the capital market is the wonderland for investors. The capital market is different from other markets in which asset partitioning creates multiple smaller assets with each having an asset value that is susceptible to information and control, this is the reason why financial organisations will take advantage of these traits to make huge profits in the capital market. Strictly speaking, short selling research organisations are adding an ‘aphrodisiac’ to market intel that confuses small and medium investors.

Notable short selling research organisations in the market include Muddy Waters Research, Glaucus Research, Citron Research, and Anonymous Analytics. These organisations have tentacles with a far reach, and once a company is targeted by a short selling research organisation, its stock price is destined to plummet without fail when a short selling report is released. As a result, short selling research organisations are often considered as the accomplices of short-sellers.

The Cost of Short Selling - The relationship between short selling research organisations and short-sellers

Before we talk about short selling research organisations, let’s start with the term ‘short selling’. What is ‘short selling’? In simple terms, short selling is when an investor predicts the price of a security asset to drop, but without owning the security, the investor borrows the target security from a securities firm or holder at an interest and sell short; and if the price drops as expected, the investor can buy back at a lower price and pay back the interest, thus profiting from the difference.

However, short selling is not applicable to all securities assets. In the Hong Kong capital market, only securities listed on the Hong Kong Stock Exchange’s ‘Designated Securities Eligible for Short Selling’ are eligible, so for a short-seller, all that needs to be done is review the list to find a target. In fact, both short-sellers and short selling research organisations live off the business of short selling, and are not much different in their nature.

In the case of Glaucus Research, it is a professional organisation that specialises in short selling reporting. The logo of the company is a ‘blue dragon’, which is a small but strong marine creature that looks like a mutated lizard. Back to what’s at hand, under its terms of service, it states that users ‘agree that use of Glaucus Research California LLC’s (“Glaucus”) research is at your own risk. In no event will you hold Glaucus or any affiliated party liable for any direct or indirect trading losses caused by any information on this site.’

As a short-seller, there is a cost to every short selling activity in terms of market condition, stock quantity, the reputation of the short-seller and the cost of interest. According to the short selling instructions on a securities firm’s website, the interest rate for short selling is agreed by both parties, and it is similar to futures in which the floating margin rate is based on mark-to-market, stock’s daily price and changing margin conditions. According to the requirement of the Hong Kong Stock Exchange, investors have to provide a collateral of at least 105% of the value of the stock borrowed, but this number might vary for different securities firms.

|

Example 1: Maintenance Margin is 115% of market value If Tencent (#00700) price rises to $110 Margin ratio = 114% [125,000 / (110*1000), lower than 115%] Since the margin ratio is lower than 115%, Margin deposit is needed. Deposit amount= $11,250 [1.25 * (109 * 1000) - 125,000]

Example 2: If Tencent (#00700) price falls to $90 Margin Ratio = 139% [125,000 / (90 * 1000), larger than 115%] No margin deposit is needed. Stock Return:

|

||||||||||||||||

Short-sellers are willing to do anything for profit. In the case of Fullshare, the company has actually experienced success in its early phase of business transformation with its new energy and healthcare sectors making great financial contribution to the company. According to inside sources, Fullshare currently has a net asset value of $30 billion and will be increased to $50 billion within the year. In addition, the company’s childcare and education division has plans to expand to markets in Australia, Beijing, and Chengdu. So, it is a huge gamble for Glaucus to target a company like Fullshare.

According to inside sources, Glaucus and other short-sellers have borrowed 950 million shares of Fullshare and sold 770 million shares at an average selling cost of HK$3, which means they still have 180 million shares (worth $23.1 billion) in hand. But if all shares were sold, it would have resulted in an income of $28.5 billion. Without taking the cost of borrowing into account, if the price of Fullshare rose to HK$3.5, short-sellers such as Glaucus would have to pay an extra HK$4.75 billion in deposit in order to repurchase the stocks to return to the borrower. In addition, if short-sellers decided to sell all shares, they still had to pay the deposit.

Short-sellers face great risks with the possible occurrence of margin calls. If the stock price of Fullshare skyrocketed and surpass the average selling cost of HK$3, short-sellers will face great loss, and have to wait for the price to drop for liquidation. However, to maintain the maintenance margin, they will be required to pay extra deposit, which will continue to increase if the stock price maintains on a rise. If the maintenance margin is not kept, short-sellers will be forced to liquidate.

The poor quality of short selling research organisations and how they stage the attack

Short-sellers will form alliances in their quest for gaining profit, and will make extensive preparations ahead of time. There is a network of organisations that stand to profit in association of short selling research companies such as Muddy Waters Research, Anonymous Analytics, and Glaucus. Before launching every attack, short-sellers would make meticulous preparations in terms of capital, position and research reports, but their focus is always Hong Kong listed companies.

Since its establishment six years ago, Muddy Waters Research has short sold seven Hong Kong listed companies, and its latest attack was during 16-19 December 2016 when it released two short selling reports on China Huishan Dairy (06863.HK). Another short selling research organisation, Citron Research, short sold the Chinese developer giant Evergrande Group on 21 June 2016, and Anonymous Analytics did it to Rexlot Holdings (00555), Hsin Chong Group (00404), and Credit China (8207).

The effects of these short selling reports vary, but the targeted company usually suffers a big drop or amplitude on the same day. For example, the price of Evergrande dropped 20% when Citron Research released its report on company, Rexlot Holding 80% with Anonymous Analytics, and Tech Pro 90% in the case of Glaucus.

In fact, short-sellers generally plan their attacks weeks ahead of time instead of waiting until the release day of the report; therefore, they do not simply profit from a one-day plummet but manage to gain a higher earning. Using the Glaucus’s short sale of Fullshare (00607) as an example, according to inside sources, Glaucus and other short-sellers already had their plan laid on 10 February 2017, but when substantial profits couldn’t be made, they published the short selling report to maximise their profits.

A 10% probability? The short selling probability of Glaucus

How do short selling research organisations pick their targets? They usually select companies that are undergoing business transformation or mergers and acquisitions, or have flaws in their finance, all of which make them vulnerable to short selling. In fact, the success of short sales relies entirely on probability, and short selling research organisations might encounter one fail out of ten listed companies. It is just like flipping a coin, there is always a 50% probability that you will get heads, and if you keep guessing heads, you will definitely get it right at least once.

Using the case of Glaucus for another example, this short-seller has short sold over 20 listed companies since 2011 which include five US-listed companies, ten Hong Kong listed companies and five listed companies from other markets. Glaucus didn’t start short selling Hong Kong listed companies until 2012, and the success rate was 10% among the ten listed companies that were short sold during the five years.

|

Date |

Target |

Same Day Gain/Loss |

Gain/Loss 3 weeks after the release of report |

Organisations with maximum fluctuation in position 3 weeks after the release of report |

Current Stock Price (HK$/share) |

|

2012.4.11 |

Shougang Fushan Resources (00639) |

-2.6% |

-28% |

HSBC Broking (+ 18 million shares), Standard Bank (-64 million shares) |

HK$1.43/share (40% drop since release of report) |

|

2012.4.24 |

1.11% |

-13% |

JP Morgan (+35.4 million shares), Standard Bank (-157.1 million shares) |

||

|

2012.8.8 |

West China Cement (02233) |

-1.58% |

-19% |

HSBC (+27.2 million shares), BNP Paribas (-56.1 million shares) |

HK$1.17/share (23% drop since release of report) |

|

2013.2.27 |

China Metal Recycling (0773) |

- |

- |

- |

Delisted on 4 February 2016 |

|

2013.10.16 |

China Child Care (01259) |

-26.09% |

-32% |

HSBC (+16.12 million shares), Deutsche Bank (-10.23 million shares) |

HK$0.46/share (93% drop since release of report) |

|

2014.3.25 |

Lumena New Materials (00067) |

-7.41% |

-17% |

BOCOM International (+813 million shares), ICBC International (-834 million shares) |

Suspension since 25 March 2014 |

|

Date |

Target |

Same Day Gain/Loss |

Gain/Loss 3 weeks after the release of report |

Organisations with maximum fluctuation in position 3 weeks after the release of report |

Current Stock Price (HK$/share) |

|

2015.2.16 |

Ozner Water (02014) |

-20.06% |

-28% |

JPMorgan Chase Bank (+19 million shares), Standard Bank (-26 million shares) |

HK$1.95/share (46% drop since release of report) |

|

2015.3.26 |

14.45% |

-17% |

|||

|

2015.4.02 |

3.27% |

-22% |

|||

|

2016.4.22 |

Real Nutriceutical (02010) |

-2.87% |

-8% |

CCB International (+238.32 million shares), Citibank N.A. (-60 million shares) |

HK$0.455/share (38% drop since release of report) |

|

2016.7.28 |

Tech Pro (03823) |

-86.34% |

-90% |

Sinopec Securities (+15.17 million shares), China Rich Securities (-19.1 million shares) |

HK$0.13/share (95% drop since release of report) |

|

2016.11.23 |

CTEG (01363) |

-12.62% |

-23% |

Citibank N.A. (+598 million shares), HSBC (-607 million shares) |

HK$1.45/share (40% drop since release of report) |

|

2016.12.01 |

-21.93% |

-40% |

Citibank N.A. (+861 million shares), HSBC (-854 million shares) |

||

|

2017.4.25 |

Fullshare (00607) |

-11.89% |

-28% |

UBS (+1.10431 billion shares), Citibank N.A. (-121.2 million shares), HSBC (-1.522 billion shares) |

Suspension since 25 April 2017 |

|

Total |

- |

-174.62% |

-365% |

- |

- |

|

Average Drop |

- |

-19.4% |

-41% |

- |

- |

Is Glaucus working alone? The answer is a definite NO because wolves travel in packs. Looking at the ten listed companies that Glaucus short sold will give us some clues. Since short-sellers have to plan ahead before the report is released in order to maximise their profit margins. Based on the charts above, organisations with the maximum fluctuation in position three weeks after the release of the report are Standard Bank, HSBC, JP Morgan, UBS[JW1] , and CITIBANK N.A。

Among these organisations, Standard Bank and HSBC had the greatest movement in their positions, but of course, these financial organisations might not be using its full position and lend some of it to other organisations, meaning that Glaucus might have association with more investment organisations than indicated in the data. In these ten instances of short selling, short-sellers gained lucrative profits from Tech Pro, which reported a 90% drop within three weeks, and CTEG 40%.

In the cases of Shougang Fushan Resources, Ozner Water, and CTEG, Glaucus decided to further raid these companies. In the first phase, CTEG experienced a 12.62% drop, and when trading was resumed seven days later, another attack was launched. However, Glaucus doesn’t win all the time, in the case of Ozner Water, its stock price dropped 20.06% in the first attack, but six months later, the price jumped 14.45% despite the second attack, and further rose 3.27% five days later when the third attack was launched.

The attack on Fullshare is proof of Glaucus’s low credibility

Let’s use the short sale of Fullshare by Glaucus as an example. When the short selling report on Fullshare was released on 25 April 2017, Fullshare filed for an immediate suspension. With this example, we can pretty much reconstruct the short selling process of short-sellers.

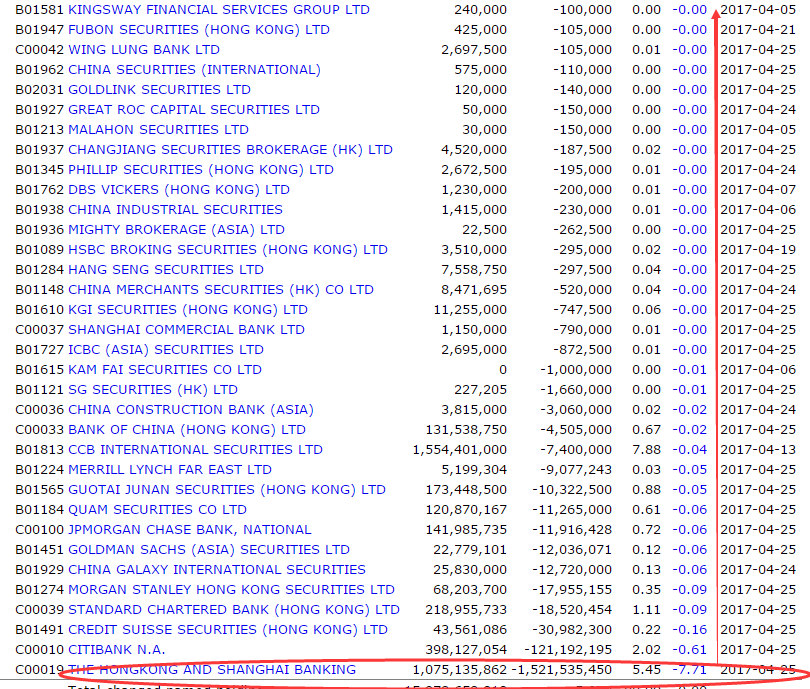

From a relevant site, we can see the position for Fullshare changes for various investment organisations. During the three-week interval after the release of the report, the position of UBS fluctuated the most at 1.10431 billion shares, and BNP Paribas came second at 397 million shares. According to the short selling process, short-sellers will wait for the stock price to drop to a level that yields a satisfactory profit margin, then buys it to give back to the borrower, meaning that UBS likely acted as a borrowing institution, but we cannot rule out the possibility that other short-sellers borrowed its position.

According to data from 25 April 2017, 1.52154 billion shares were reduced from HSBC’s position which accounted for 7.7% of total shares issued, and 417.23 million shares more than UBS’s position. These data can either be seen as proof of the activities of short-sellers or ordinary transactions. Comparing the position change of UBS and HSBC, we can deduce that UBS has already made a profit from short selling but not HSBC.

If this insider data is accurate, short-sellers made a total profit of HK$950 million before the suspension of Fullshare. With a 5x leverage ratio and 10% financing cost, the net profit is at least HK$722 million. If Glaucus was to receive a percentage, it would amount to HK$72.2 million at 10%, making it even more profitable than robbing a bank!

In summary, short selling research organisations attacked listed companies to make money, and their success relies entirely on a probability that has no foundation. In the case of Glaucus, only one of the ten listed companies was delisted, that is a very low ratio to even establish any credibility. Since various evidences indicate that short selling reports are created with a specific purpose to rip off companies, and small and medium investors, short selling research organisations have a low credibility and should not be trusted.

Finally, investors should see Fullshare’s retaliation as a step to fighting back the malicious acts of short-sellers!

Disclaimer

The information contained on this article is intended solely to provide general guidance on matters of interest for the personal use of the reader, who accepts full responsibility for its use. The application and impact of laws can vary widely based on the specific facts involved. Given the changing nature of laws, rules and regulations there may be delays, omissions or inaccuracies in information contained on this article. Accordingly, the information on this article is provided with the understanding that the author and publisher are not herein engaged in rendering professional advice or services. As such, it should not be used as a substitute for consultation with a competent adviser. Before making any decision or taking any action, the reader should always consult a professional adviser relating to the relevant article posting.

While every attempt has been made to ensure that the information contained on this article has been obtained from reliable sources, there is not responsible for any errors or omissions, or for the results obtained from the use of this information. All information on this article is provided "as is", with no guarantee of completeness, accuracy, timeliness or of the results obtained from the use of this information, and without warranty of any kind, express or implied, including, but not limited to warranties of performance, merchantability and fitness for a particular purpose. Nothing herein shall to any extent substitute for the independent investigations and the sound technical and business judgment of the reader. In no event will the author / publisher, or its partners, employees or agents, be liable to the reader or anyone else for any decision made or action taken in reliance on the information on this article or for any consequential, special or similar damages, even if advised of the possibility of such damages.

Links to Related Internet Sites

From time to time certain links may be posted on this article connecting readers to third party web sites. The author / publisher does not accept any responsibility for, nor makes any representations as to the accuracy of, any content in such third party web sites.

Third Party Comments

Third parties may submit comments for publication on this article. Any such comments are submitted on the basis that the author / publisher will review and may edit such comments, and that not all submissions will be published. Any third party comments published on this article (whether edited or not) are third party information for which the author / publisher takes no responsibility and disclaims all liability, and the above disclaimer applies to any such third party comments.

[JW1]DELETE SPACE