After its 17.46% and 14.87% rise on 4 May and 5 May 2017 respectively, Fullshare (00607-HK)started trade on 8 May 2017 with a further increase of 2% to HK$3.46. Since its resumption on 4 May, the stock price of the company skyrocketed 37.3% within just three trading days. As a result, after borrowing 950 million shares at a selling cost of HK$3, short-sellers have already lost HK$437 million based on today’s opening price of HK$3.46, even without taking the interest rate into account.

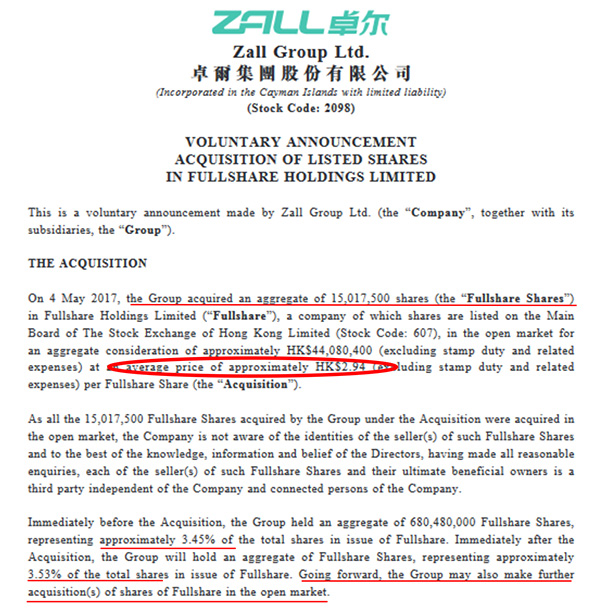

Fullshare decided to buyback its shares in retaliation of the short-sellers’ attack, and this move has acted as a display of the company’s confidence in its own development, and at the same time, will minimise the number of shares short-sellers can sell as the price of Fullshare has already surpassed the selling cost of short-sellers. Furthermore, on 5 May 2017, Zall Development announced that it had acquired 15,017,500 shares of Fullshare at an average price of HK$2.94 in the open market, increasing its stake from 3.45% to 3.53%, and there may be further acquisition of shares in the open market, which serves as an indication of Zall Development’s faith in Fullshare.

Fullshare’s business transformation to platform-based with diversification

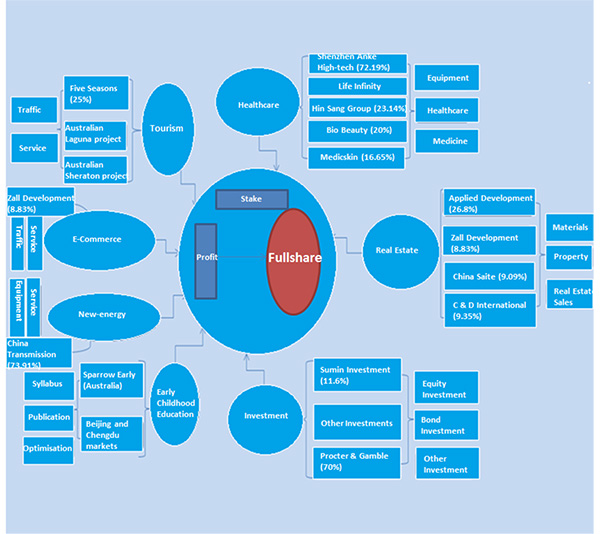

The value of Fullshare is widely recognised by market investors because of its strategic development in its businesses. As of the information derived from its 2016 annual report, Fullshare’s current businesses include five major categories: real estate, new energy, healthcare, tourism, and investment. In fact, Fullshare has transformed itself into a platform-based enterprise with diversified businesses, and the company has plans to make its mark in the early childhood education and e-commerce sectors.

The above chart illustrates the business structure of Fullshare (as of the information derived from fullshare’s annual report). The platform-based model is actually developed on the basis of shareholding or stakeholding, rather than a wholly-owned business, which is how Fullshare currently operates its seven major businesses. This chart does not only show the business map of Fullshare, but also its profit roadmap, illustrating how its holding companies continuously generate profit for Fullshare.

The advantage of platform investment comes from the utilisation of capital from holding companies to generate profit; however, Fullshare is more than that, as the company also has its own businesses,real estate is still the core business of Fullshare at of this moment, and the company had acquired related companies in 2016, but it may be developed more base on the platform-based business in future. It is worth mentioning that the platform-based model isgood for business expansion and can efficiently disperse risks.

The two moneymakers

Considering the seven businesses that Fullshare currently holds, real estate is comparatively more traditional, but it provides more constant gross profit which has been steadily kept at 20%. Comparatively, the new energy and healthcare sectors offer higher gross profit which reached 37% and 35% respectively according to Fullshare’s 2016 annual report. Fullshare’s investments pull in new sources of income, one example is its holdings of Zall Development, which is a smart e-commerce business, definitely has bright future.

Fullshare started its new energy sector at the end of 2016, when it obtained a 73.91% stake of China Transmission through share exchange. China Transmission has a high profit margin and high profit growth rate, and the company had a net profit of RMB1.11 billion in 2016 which made the average three-year growth rate at 208%. It was able to enjoy such high profit due to its oligopoly position and market share in the industry.

According to China Transmission’s 2016 annual report, the company’s main products is wind-powered transmission equipment, which possesses 29% of the market share globally. With only a few large-scale enterprises in the same business, China Transmission has an oligopoly in the market, and thus, the company doesn’t face any risk in product management and customer assessment, and has an advantage in pricing because of its large market share.

The smart e-commerce business is operated through its holding company Zall Development, while real estate is also one of the Zall’s business. Zall Development is looking into changing its business model. In 2016, Zall Development acquired international e-commerce platform, LightInTheBox, and the Mainland’s largest agricultural product e-commerce company, Shenzhen Agricultural Product, with the intention to build up a world’s largest B2B trading platform and database. At the same time, the company is also building a payment service platform to complement its trading platform. In 2016, Zall Development had a net profit of RMB2.057 billion.

According to its company profile, Shenzhen Agricultural Product has transformed from trading a single commodity to multi-commodity and diversified business, and that allow it has quickly become the Mainland’s largest B2B e-commerce platform in agricultural products with daily transactions in the millions. If Shenzhen Agricultural Product can take advantage of its huge traffic, and fully utilise the payment service platform that Zall Development provided, the business can obtain its market share in the payment service business and become the ‘Alipay’ of the agriculture sector.

Short collection period with high income to provide sufficient cashflow for expansion

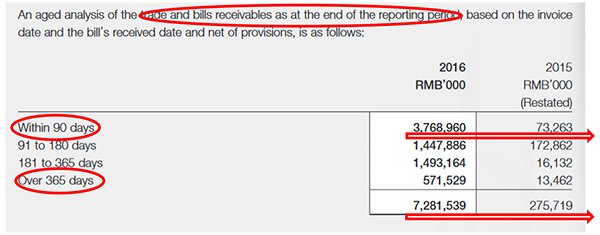

Looking at Fullshare’s overall business income. In Fullshare’s 2016 annual report, we can find an analysis of the company’s trade and bills receivables, which can act as the basis to determine its quality of income. Fullshare had RMB3.769 billion in bills receivables within 90 days, which had a year-on-year growth of 50.44 times, and the bills receivables over a year was RMB571,530,000 which only took up 7.8% of total bills receivables.

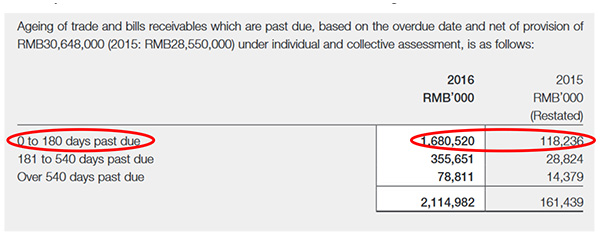

Fullshare had a cashflow of RMB3.864 billion in 2016, and adding the bills receivables within 90 days, the total cashflow was RMB7.633 billion, which is a pretty good quality of income. However, these receivables might be overdue if a client could not pay on time. In 2016, Fullshare had a total of RMB1.68 billion in bills receivables over 180 days, which was 79.4% of all bills receivables, indicating the amount of overdue accounts was not too great.

It can be assessed that Fullshare’s cashflow mainly comes from bills receivables within 90 days and receivables, and when combined, they provide the company with sufficient cashflow for investment. Since the company’s transformation to platform-based, Fullshare is putting more effort in boosting its investment quality, especially in the area of enterprise equity investment. Fullshare is currently operating seven businesses, but there is no telling if it will invest or expand into other businesses with a higher gross profit and growth potential.

It is worth mentioning that Shenzhen Anke High-tech from the healthcare sector, and China Transmission from the new energy sector possess a strategic advantage as they are both high technology enterprises. According to Fullshare’s 2016 annual report, the company has four subsidiaries that are subjected to tax at a preferential rate of 15% which is 10% less than usual tax rate. Amongst them, Shenzhen Anke High-tech, Nanjing High Accurate Drive, and C Transmission all received their approval in 2015, so they can still enjoy the preferential tax rate this year which injet extra cashflow to Fullshare.

|

Disclaimer

The information contained on this article is intended solely to provide general guidance on matters of interest for the personal use of the reader, who accepts full responsibility for its use. The application and impact of laws can vary widely based on the specific facts involved. Given the changing nature of laws, rules and regulations there may be delays, omissions or inaccuracies in information contained on this article. Accordingly, the information on this article is provided with the understanding that the author and publisher are not herein engaged in rendering professional advice or services. As such, it should not be used as a substitute for consultation with a competent adviser. Before making any decision or taking any action, the reader should always consult a professional adviser relating to the relevant article posting.

While every attempt has been made to ensure that the information contained on this article has been obtained from reliable sources, there is not responsible for any errors or omissions, or for the results obtained from the use of this information. All information on this article is provided "as is", with no guarantee of completeness, accuracy, timeliness or of the results obtained from the use of this information, and without warranty of any kind, express or implied, including, but not limited to warranties of performance, merchantability and fitness for a particular purpose. Nothing herein shall to any extent substitute for the independent investigations and the sound technical and business judgment of the reader. In no event will the author / publisher, or its partners, employees or agents, be liable to the reader or anyone else for any decision made or action taken in reliance on the information on this article or for any consequential, special or similar damages, even if advised of the possibility of such damages.

Links to Related Internet Sites

From time to time certain links may be posted on this article connecting readers to third party web sites. The author / publisher does not accept any responsibility for, nor makes any representations as to the accuracy of, any content in such third party web sites. Third Party Comments

Third parties may submit comments for publication on this article. Any such comments are submitted on the basis that the author / publisher will review and may edit such comments, and that not all submissions will be published. Any third party comments published on this article (whether edited or not) are third party

information for which the author / publisher takes no responsibility and disclaims all liability, and the above disclaimer applies to any such third party comments. |

-----------------------------------------------------------------------------------------------------------------------------------------

Media Contacts:

Sunny Wan

+852 2153 7297 / sunnywan@finet.com.hk

Wells Pan

+ 852 6925 6988